How do I choose and apply for a credit card?

Credit cards are the easiest way to build your credit but they can ALSO help you shop and travel smart. It’s hard to get your first card when your credit history is limited, but you have a few options.

Only if you use them to buy things you can’t afford and then don’t pay off the bill at the end of the month — that will hurt your credit and put you in debt. BUT, if you use credit cards to buy things you’d normally buy anyways and pay them off fully every.single.month, they’re not bad at all.

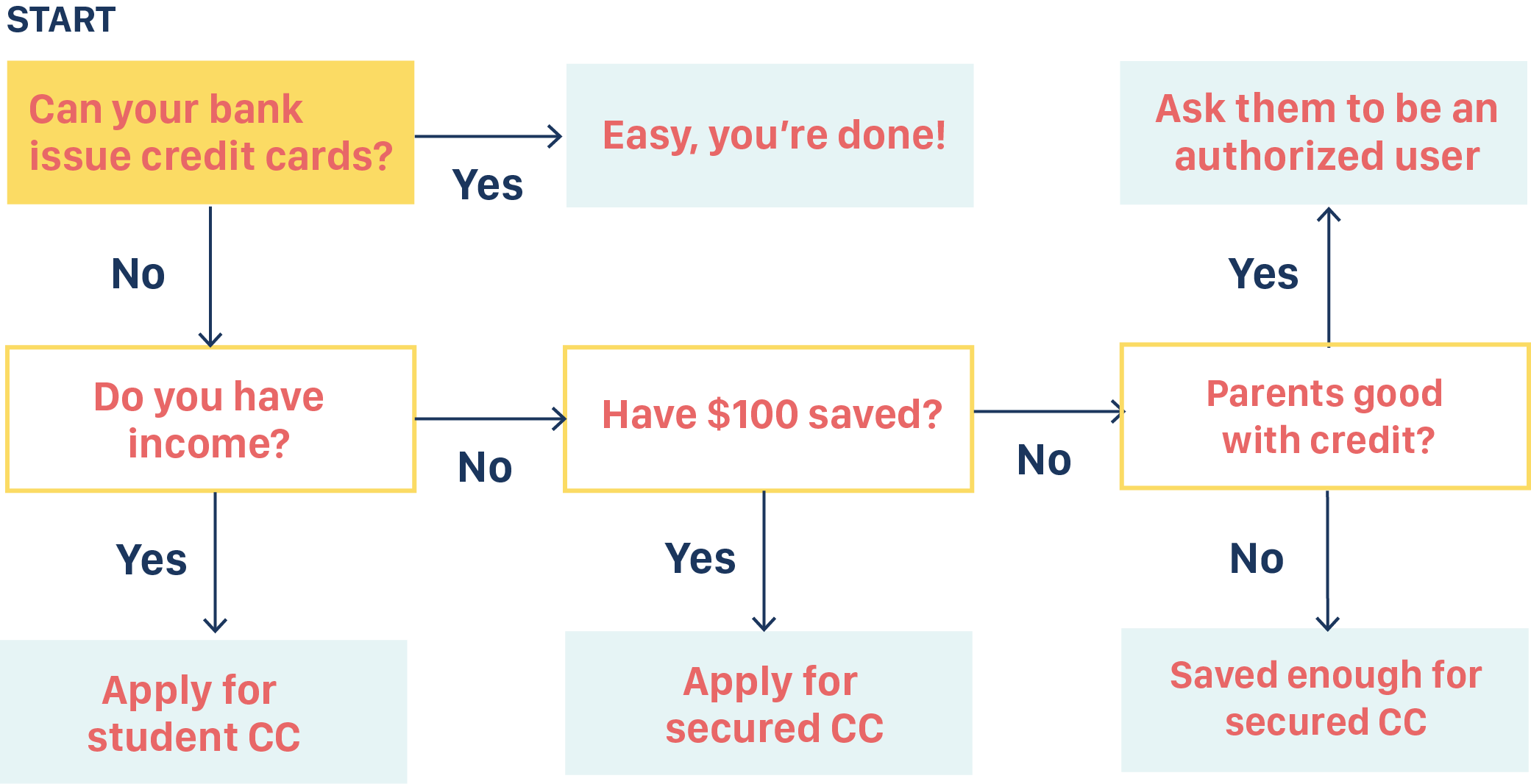

A plain-vanilla one.🍦Don’t worry about perks like points and cash-back for now. (If you’re new to credit, you likely won’t get approved for the bells-and-whistles cards. Those come after you build good credit, which, because you are reading this, you’re on your way to do!) Right now, focus on getting a basic card to start proving that you can use credit responsibly. If your bank can issue you one, that’s ideal. Otherwise, look into the following options, which are designed for people who have a limited credit history.

A card that’s designed for students who are new to credit. They can be easier to qualify for than “regular” cards (card companies look past your lack of credit history because they know you’re in college, which means you’re on track to being a successful and responsible borrower). To qualify, you usually need to prove you have an income (a part-time job works).

A starter card that requires a deposit (a few hundred bucks) to protect the bank in case you don’t pay your bills. Your credit limit (the max you can spend) equals the deposit. This is a way to build credit if the other options don’t work for you. Plus, you can get the deposit back by upgrading the card to a “regular” card once you prove you’re good for it. (By then, that’s basically free money you can save or invest.)

Someone who can spend on a card but isn’t ultimately responsible for the bill. If you’re an authorized user on a parent’s card, their good credit will rub off on your credit — assuming they always make on-time payments and that the card company reports to the credit bureaus (the companies that make credit reports) on your behalf.